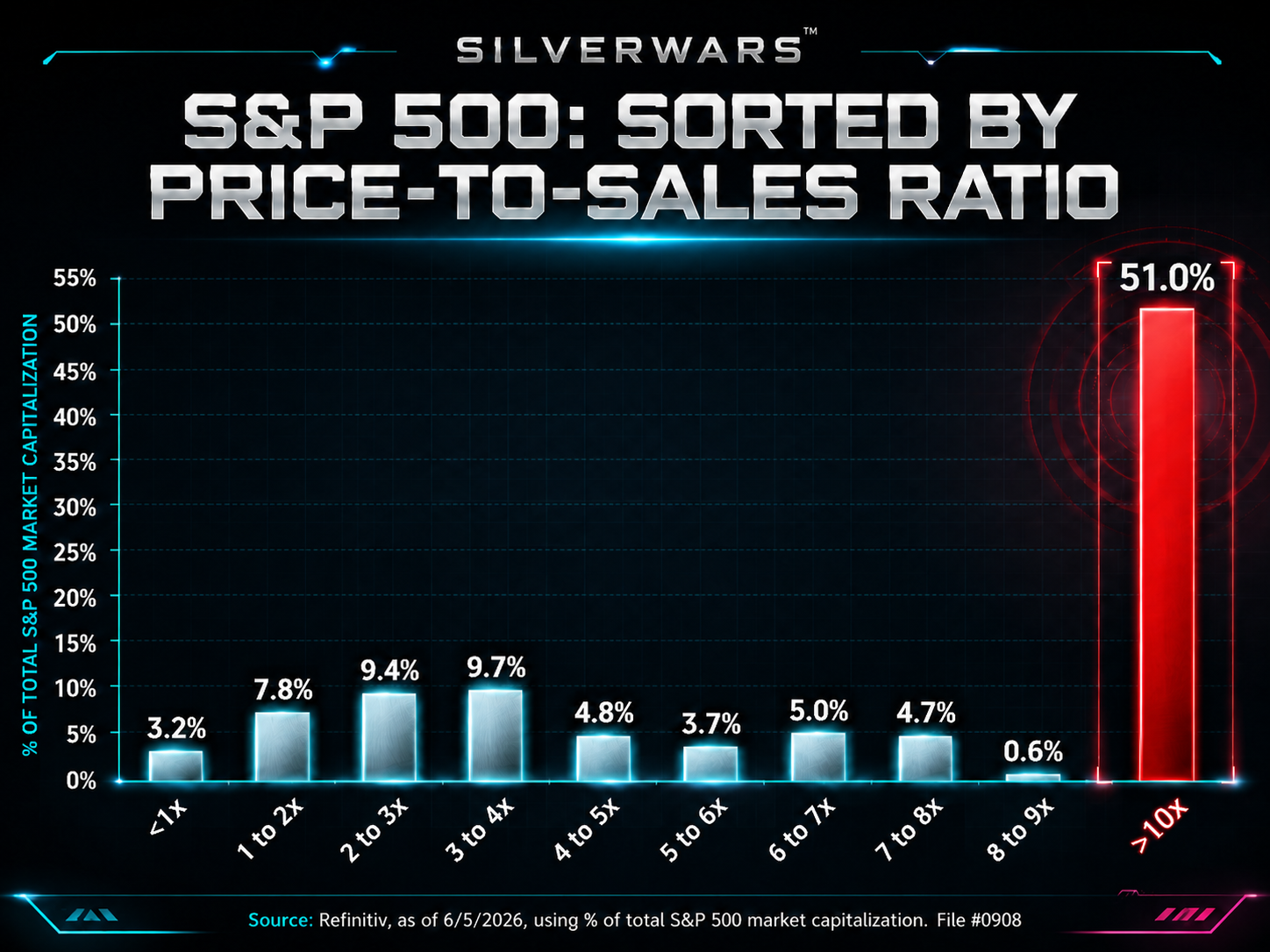

Half the S&P 500’s market value is now in stocks trading above 10 times sales.

Not profits. Not free cash flow. Sales.

A chart using Refinitiv data dated June 5 shows 51% of the index’s market cap sitting above that line. That is not a speculative pocket of the market. That is not a handful of weird names with cartoon valuations. That is half the index.

The market did not forget the dot-com bubble. It looked at the warning label and said, “Run it back.”

The old quote still matters because the math has not changed. After Sun Microsystems collapsed from its dot-com peak, CEO Scott McNealy explained how absurd the valuation had been. At 10 times revenue, he said, investors basically needed the company to pay out 100% of revenue for 10 straight years to get their money back. No costs. No taxes. No employees. No research. Just every dollar of sales handed back to shareholders.

Then he asked the only question that mattered:

“What were you thinking?”

That was Sun Microsystems at roughly 10 times sales.

Today, half the S&P 500 is there.

And yes, people will immediately say the obvious thing. These companies are better. They have cloud revenue. AI demand. Chips. Software margins. Network effects. Buybacks. Cash. Real products. Real customers.

Sure.

Cisco was real too.

Microsoft was real. Intel was real. Qualcomm was real. Amazon was extremely real. The internet was not fake. The problem was never that the technology did not matter. The problem was that investors paid prices that required the future to arrive perfectly, on time, with no potholes, no margin pressure, no rate shock, no competition, and no executive saying something stupid on an earnings call.

That is not investing. That is buying a flawless timeline.

Look at what happened to the dot-com survivors. Cisco traded around 25 times sales and fell about 90%. Microsoft got cut in half and then some. Intel took roughly a generation to fully recover its old peak. Amazon became one of the greatest companies in history and still dropped about 97% before the long-term story bailed out anyone with the stomach to hold.

That is the part people hate hearing.

A great company can still be a terrible stock if you pay a stupid price.

The losers were uglier. Sun Microsystems crashed and was eventually sold. JDSU got shredded. Yahoo fell apart. Lucent basically disappeared into telecom rubble. Nortel went bankrupt. That was the graveyard around the winners.

So when someone says, “This time is different because AI is real,” the answer is simple: so was the internet.

The danger is not that every expensive stock is fake. That is lazy. The danger is that investors have started treating a real boom like it has no price limit. AI demand can be enormous. Data centers can grow. Semiconductor revenue can keep rising. None of that automatically makes 10, 20, or 30 times sales a good entry point.

Valuation is not a vibe check. It is the bill.

And right now, the bill is large.

This is where the chart gets uncomfortable. If 51% of the S&P 500’s value is above 10 times sales, then the broad market is no longer just “expensive.” It is leaning on a small group of companies priced for very little disappointment.

That matters because disappointment does not need to be dramatic at these levels. Earnings do not have to collapse. AI does not have to fail. The economy does not have to implode.

The market just has to realize it paid 2035 prices in 2026.

That is how bubbles hurt people. They do not always sell a fake product. Sometimes they sell the right product at the wrong price to everyone at the same time.

Different decade. Same math.